Insurance Roof Replacement: Understanding Depreciation

Dealing with a damaged roof can be stressful, especially when insurance is involved. One of the most common points of contention between homeowners and insurance companies is depreciation. Understanding how depreciation affects your roof replacement claim is crucial to ensuring a fair settlement. This article will delve into the complexities of depreciation in insurance claims for roof replacement, helping you navigate this often-confusing process.

What is Depreciation in Insurance Claims?

Depreciation, in the context of insurance, refers to the reduction in the value of your roof over time due to age and wear and tear. Insurance companies consider depreciation when calculating the amount they will pay for repairs or replacement. Essentially, they argue that since your roof wasn't brand new when the damage occurred, they shouldn't have to pay for a completely new roof. They deduct the depreciation amount from the Actual Cash Value (ACV) of your roof, leaving you with a potentially significant shortfall.

How is Depreciation Calculated?

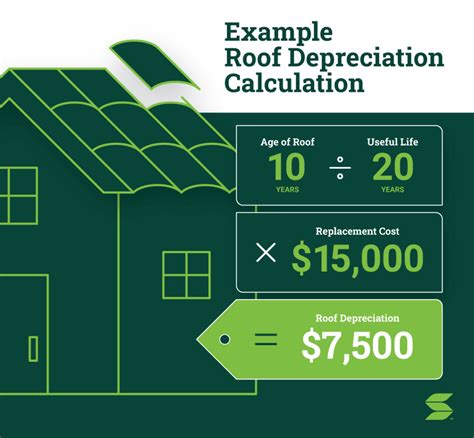

The method for calculating depreciation varies by insurance company and state, but it typically involves estimating the roof's lifespan and the percentage of its life that has already passed. For example, a 20-year-old roof with a 25-year lifespan would be considered 80% depreciated (20 years/25 years). The insurance company would then deduct this percentage from the replacement cost to arrive at the ACV. Some companies use a straight-line depreciation method, while others may utilize more complex formulas. It's important to carefully review your policy and contact your insurer to understand their specific approach.

What is Actual Cash Value (ACV)?

ACV is the market value of your roof, considering its age and condition at the time of damage. This differs from Replacement Cost Value (RCV), which represents the cost of replacing your roof with a comparable new roof. ACV is generally lower than RCV because of depreciation. Most insurance policies will initially offer you the ACV for the damage.

Can I Avoid Depreciation on My Roof Replacement Claim?

While you can't entirely avoid depreciation under most standard insurance policies, you can mitigate its impact. Several strategies might help:

1. Review Your Policy Thoroughly:

Carefully examine your insurance policy to understand its specific depreciation guidelines. Some policies might offer options to reduce or eliminate depreciation, such as endorsements or riders.

2. Document Your Roof's Condition:

Maintaining thorough records of your roof's maintenance and any previous repairs can strengthen your claim. Photos and documentation of regular inspections can prove the roof was in good condition before the damage.

3. Negotiate with Your Insurance Company:

Don't hesitate to negotiate with your insurance adjuster. Present a strong case, supported by documentation, and explain why a full replacement is necessary rather than a partial settlement based on ACV. Sometimes, a higher settlement can be reached through amicable negotiations.

4. Consider Replacement Cost Value (RCV):

Some policies offer coverage for RCV rather than ACV, which eliminates depreciation. Inquire about the possibility of adding an RCV endorsement to your policy.

What if I Have an Older Roof?

Depreciation becomes a more significant concern with older roofs. The higher the percentage of depreciation, the larger the gap between ACV and RCV. For very old roofs, securing a full replacement through insurance can be challenging.

How Can I Get the Best Outcome?

- Hire a Public Adjuster: A public adjuster is a professional who represents you in your insurance claim. They have expertise in negotiating with insurance companies and can help you secure a more favorable settlement.

- Obtain Multiple Estimates: Get quotes from several reputable roofing contractors to support your claim and show the true cost of replacement.

- Keep Detailed Records: Maintain comprehensive records of all communication, documents, and estimates related to your claim.

Understanding depreciation is crucial for navigating insurance claims for roof replacement. By understanding the process, documenting your roof's condition, and negotiating effectively, you can increase your chances of receiving a fair settlement. Remember, your insurance policy is a contract, and you have rights. Don’t hesitate to seek professional assistance if you need help understanding your policy or negotiating with your insurance company.